In our previous post, on Distribution, we pointed out that claims represents perhaps the most important customer touchpoint in the entire insurance journey.

But claims is even bigger still – Nothing affects carriers’ bottom lines like claims; too many are not just capable of wiping out company margins but can jeopardise company survival full stop. And it’s not as if customers like claims either… If insurers could magically prevent the underlying events from happening, customers – fraudsters aside! – would always prefer this.

And speaking of fraudsters, further ahead in this article we will take a closer look at fraudulent claims which are also a massive area of carrier losses. There is a tricky balance to be struck here... Treating every claimant like a potential criminal is an obvious no-no, but objective scrutiny must exist at some point in the policy life-cycle.

Claims

There are in principle two key thrusts – Claims Prevention & Mitigation and Customer Experience in Claims – which we shall now explore. The stats and perspectives below are taken from our Global Trend Map; a full breakdown of our survey respondents, and details of our methodology, are included as part of the full report, which you can download for free at any time.

In theory, the scope for claims prevention and mitigation has been radically widened thanks to the Internet of Things, which does not just allow for better underwriting (by netting more data and feeding predictive models) but can also empower insurers – or other ecosystem players too, for that matter – to intervene when things point towards an impending claim event. Claims, in the sense of claims prevention, is fast coming under the strategic spotlight as a means to shelter exposed policyholders, rescue broken policy portfolios and shore up insurers stricken by low interest rates and bad risk.

Another benefit of sensor data is real-time insight into what has actually gone on with a claim event, which can be life-saving in an accident-and-emergency context, keeps a lid on damages at the point where they are liable to spiral the most and helps to identify cases of fraud.

"Claims is a significant part of the insurance value chain and, in our view, offers the largest potential for innovation. Many insurers are struggling with the dynamic of reducing costs whilst providing a positive customer experience. Recently in the US and the UK, many of the large insurers have experienced significant underwriting losses, for core products like motor, due to poor claims experience, deteriorating driving behaviour, and rising repair/medical costs."

Sam Evans, Managing Director at Eos Venture Partners

While prevention does continue to get better, accidents and unforeseen incidents are always going to occur, so claims certainly aren’t going away anytime soon. It is here as well that the claims department can be a strategic differentiator for carriers. When a claim occurs, insurers have the opportunity to impress their customers at that precise moment when those customers need, and appreciate, their insurance the most.

We have noted throughout this content series (for instance in our earlier post on Insurer Priorities) the growing importance of customer-centricity to insurers. And claims – as the key, and in some cases only, consumer touchpoint – has become a key avenue of engagement. If insurers can provide excellent customer service throughout the claims experience, removing friction from the process wherever they can, then they are more likely to retain their policyholders’ custom and even open cross-selling opportunities.

1. Customer Experience in Claims

Is customer experience (CX) a core focus for claims departments?

We asked carriers whether customer experience (CX) was a key factor within their claims departments, and in total 69% replied ‘yes’ and 26% ‘somewhat’. The trend we alluded to above – of the growing importance of customer-centricity within every insurance function – is therefore borne out handsomely by the statistics.

Looking across our lines, we see a consistently high focus on CX in claims, except for in Life, which trails somewhat. This probably reflects a historic lack of touchpoints (often just policy renewals and death!) and, as an extension of this, the more limited new business and cross-selling opportunities. We encountered a similar lag with this line in our earlier installment on Marketing and Customer-Centricity.

"Will claims call centres evolve from the current model of large numbers of people predominantly performing standard operations and having scripted conversations to a much smaller number of ‘problem solvers’ being available to support customers when something out-of-the-ordinary creates an exception in the automated processes?"

Ian Thompson, EMEA Chief Claims Officer at Zurich

Does automation play a role in the claims-handling process?

Customers want frictionless experiences when making a claim. Certainly most young claimants (digital natives) would prefer to do everything through an app or portal rather than filling out paper forms, and this has seen some insurers embrace non-traditional channels such as WhatsApp for submitting claims materials. In addition to slickness, customers want speed, or, where speed is not possible, clarity as to their claim's status.

This level of service can only be provided effectively through recourse to automation in some degree – so that a large portion of uncomplicated claims can be processed straight-through and the customer either notified of the outcome or given a resolution date, all at the click of a button. 46% of carriers indicated that they have an automated claims-handling process, a figure we expect to become a majority in the near future. To clarify: this stat does not necessarily imply that the majority of claims will soon be automated, merely that automation will soon be in the mix for the majority of carriers.

"There is no doubt that insurance in general, and claims in particular, will see significant changes through the automation of knowledge work. Customer choice and the importance to the customer of the claims service will mean that human involvement in the process will always be necessary. However, as claims leaders, we will need to rethink our operating models in the light of emerging technology."

Ian Thompson, EMEA Chief Claims Officer at Zurich

There are many different workflows for claims management (depending on the type and complexity of the claim, as well as its value), and claims automation generally only means automating some of these. And while automation has connotations of cost-cutting (and this is definitely still a factor), it can also be argued that less staff time spent on routine claims entails more staff time for high-stakes claims, meaning claims management can become customer-driven rather than process-driven.

2. Claims Prevention & Mitigation

How much focus do (re)insurers have on claims loss mitigation?

We asked carriers about their level of focus on claims loss mitigation, and in total 57% replied that they had ‘a lot’ and 39% ‘some’ focus. We noted that North America leads our other regions in terms of having ‘a lot’ of focus. We further explore the specificity of the North American insurance market in our forthcoming Regional Profile on the continent, which you can, of course, access immediately by downloading the full Trend Map – available to all comers free of charge.

Will IoT impact the claims department?

IoT fundamentally allows carriers (and other ecosystem players, in cooperation but also in competition with insurers!) to move from risk management to risk prevention by providing insights to actively bring down policyholder risk. In this sense, the overriding impact of IoT on claims is the reduction – or even outright elimination – of claims ...

This end goal is perfectly aligned with customer wishes, and there are many more ways IoT can boost customer-centricity in claims. If event data can be captured automatically, then this doesn’t just help eliminate fraudulent claims (which ultimately cost law-abiding customers), it also removes a lot of friction from the process of filing claims and means that business-as-usual can be resumed as early as possible.

An example of this would be a temperature-sensitive cargo insured against temperature rises above a certain point, whereby a temperature sensor – in conjunction with Blockchain and Smart Contracts – could trigger claims automatically if the limit were exceeded. This way, mitigation could begin straightaway with minimal head-scratching; in this example, that might involve immediately re-ordering the compromised cargo.

In our earlier section on Internet of Things, 60% of respondents selected Claims as one of the departments that would benefit the most from IoT, and this is largely borne out in the responses of carriers here: 53% of insurers and reinsurers believe that IoT will impact their claims department ...

Among our lines, IoT impact on claims trails in Life, unsurprisingly given that IoT-enabled Life programmes – if they exist at all – generally sit behind connected health initiatives (which get the plaudits). As the cost of sensors and connected devices continues to fall, we expect to see further growth in the connected-claims universe to the benefit of customers and carriers alike, across all lines.

While the potential of sensor-led approaches to manage down risk remains hypothetical for many use cases (there are simply not enough long-term studies yet), and there are inevitably other well-positioned ecosystem players with a shot at the prize, a more immediately tangible IoT-enabled saving is in relation to Fraud. Telematics providers may not, in the end, make you a better driver – but the g-forces can tell them exactly what has gone on with your car. And with your insurer as it were in the passenger seat, you will feel rather less able to lie to them ...

Fraud

Fraud is the dark matter of the insurance universe. Discovered cases cost insurers (and ultimately policyholders too) millions every year, and its full hidden extent can only be guessed at – it is in some sense the gap between how risk models should work and how they appear to work on the ground, with undiscovered fraud ultimately getting priced into premium costs.

Derek Brink, VP and Research Fellow in Information Security and IT GRC at Aberdeen Group, recently estimated the cost of fraud at between 5% and 10% of insurers’ annual revenue, noting also that it takes firms a median time of 20 months to detect on-going fraud. Every penny saved on fraud is an additional penny back onto insurers’ bottom lines, and what defeating fraud would ultimately mean is that they could offer their policyholders more competitive prices.

"Fraud concern is no newcomer to the insurance industry, especially in the healthcare and motor lines of business. The fact that the internet is not attributable has made the fraud situation even worse as digitisation proceeds at a pace."

David Piesse, Chairman of IIS Ambassadors and Ambassador Asia Pacific at International Insurance Society (IIS)

In this post, we assess both the size of the fraud problem and a range of approaches for containing it. The following stats and outside perspectives are drawn from our Global Trend Map; a breakdown of all survey respondents, and details of our methodology, are included in the full report, which you can download for free whenever you please.

Who Wields the Sword in the Battle with Fraud?

People most readily associate insurance counter-fraud with the claims department, because this is where fraudsters cash in and has historically been the point in the cycle where most frauds get unmasked. However, there is a limit to how far reactive approaches to fraud can take insurers, and stopping fraud closer to its roots is certainly preferable to focusing exclusively on the ‘final mile’ (namely claims) for its interception.

It’s clear that the next generation of counter-fraud will be proactive and cross-functional, tracking potential fraud indicators across the entire insurance lifecycle. We asked insurance carriers to indicate which departments were currently involved in combating fraud within their organisations ...

Understandably, we see a large role attributed to dedicated Fraud departments as well as to Claims departments, and this is unlikely to change moving forwards (the less than 100% figure for Fraud departments may be due to the counter-fraud function sometimes being subsumed elsewhere). Other departments that stand out as having central roles are Senior Leadership, Operations, Analytics, Underwriting and Risk.

"If you stop fraudsters coming into the business in the first place then you have to spend less from the beginning, enabling you to improve the journey for other, genuine customers. But it’s difficult to get that balance in a competitive marketplace as the investment isn’t so obvious. It requires a change of mind-set."

John Beadle, Head of Counter Fraud and Financial Crime, RSA

The fight against fraud is by no means limited just to carriers. Indeed, with the shift towards more proactive counter-fraud approaches, greater attention is being brought to bear on indirect channels. Historically, brokers and affiliate partners have been incentivised primarily on a volume basis and have directed plenty of bad business towards carriers. Insurers can therefore make substantial savings by educating their brokers and affiliates on best practice, so as to root out fraud at the application stage before it ever enters their wheelhouse – although they obviously need to tread a fine line between on-boarding bad business and turning away good customers.

"Part of the problem is the appetite for fraud detection in the broker channel. We’ve had to convince brokers to protect us against fraud because by sending us that business, they ultimately end up suffering too. Brokers see sales as a volume and growth business rather than one built on quality, and as a company, we are always interested in quality."

Steve Jackson, Head of Financial Crime at Covéa Insurance

A couple of general stats ...

- An overwhelming majority (92%) of our carrier respondents believed fraud is increasing, and we saw a similar level of concern from the rest of the industry.

- 29% of carriers believe that the majority of insurance fraud goes undetected, and 59% believe that some insurance fraud goes undetected (12% don’t know). The rest of the industry are in line with this assessment.

Slaying the Dragon: Approaches for Defeating Fraud

We don't have scope here to explore specific counter-fraud solutions in detail. However, we did ask our respondents and industry contributors about different high-level approaches. These include before-the-claim strategies, data-sharing coalitions, the Internet of Things (IoT) and Blockchain technologies.

"We can look at using smart technologies that look at probability and profiles of individuals’ past behaviours. If someone fits a certain profile, there is a higher probability they will be a fraudster. It’s an interesting area but also dangerous."

Steve Jackson, Head of Financial Crime at Covéa Insurance

i) Before-the-Claim Strategies

By identifying policies intended to facilitate fraud at the time of underwriting, insurers can prevent fraud advancing to the point of a claim being made; as a general rule, the more relevant data that can be pre-populated, the fewer opportunities there are for opportunistic fraudsters at the application stage. This directly reduces the amount of fraud that gets through the lines and helps also to unburden the claims department. Encouragingly:

Two thirds of Insurers & Reinsurers indicated that they had a before-the-claim fraud strategy …

ii) Data-Sharing

Fraudsters do not just recycle specific items of (fraudulent) data but also deploy the same distinctive methodologies against multiple targets. Effective data-sharing in counter-fraud means that, once unmasked, a fraud tactic is truly disarmed. Reassuringly then, we registered universal approval for this sort of initiative from the entire industry.

94% of Insurers & Reinsurers are in favour of a data-sharing coalition to prevent fraud …

iii) Internet of Things

When it comes to IoT, much of the attention is on preventative and value-added services (check out our earlier post on the topic). However, one of the more immediate boons of the technology is its role as a fraud deterrent.

Take workers' compensation insurance in a factory or construction environment, for example. Installing IoT devices on site for monitoring purposes makes it much more difficult to dress up instances of non-compliance for the purpose of inflating a claim (or making one in the first place), and means compliant clients can be treated accordingly. This also applies to the personal lines: with full transparency over where a car has been and what motions it has undergone, Auto customers are, generally speaking, less likely to lie about, and exaggerate, what has happened.

At the same time though, IoT can also be a new attack vector for fraud. By hacking an IoT device, you could in theory 'spoof' whatever behaviour you wanted, so as to deceive your insurer – which would be particularly attractive if target-based discounts were in play. Imagine hacking your FitBit to show 10km of jogging a day while you remain safely ensconced before your television awaiting your health-insurance rewards... So cybersecurity is as important for the insurance aspect of IoT as it is for every other.

iv) Blockchain

Another multi-faceted technology with clear applications for counter-fraud is Blockchain: a distributed ledger for recording transactions between different parties without relying on a trusted (though oftentimes untrustworthy) central authority for verification. We spoke briefly to David Piesse, Chairman of IIS Ambassadors and Ambassador Asia Pacific at the International Insurance Society (IIS), to find out more:

‘The emergence of the new Internet, commonly called the Blockchain, means we no longer have to trust the internet but in fact can make sure it tells the truth. In Estonia, they wrapped the internet with a Blockchain technology that has removed digital fraud from the healthcare sector in that country, and this is now being applied elsewhere.

It’s possible to map the Blockchain protocol over the Insurance Combined Ratio, with fraud and expense reduction on the top line and an increase in Earned Premium on the bottom line via new product and operational efficiency. This can give the c-suite an opportunity to see the effect of the new technology on their profitability before investment income.’

Blockchain continues its march into insurance apace. Indeed, Munich Re and Swiss Re last October founded the B3i Consortium with the express intention to ‘explore the potential of distributed ledger technologies to better serve clients through faster, more convenient and secure services.’ Blockchain clearly has massive implications for all forms of data and monetary interchange, and we look forward to seeing its continued application both in counter-fraud and more widely.

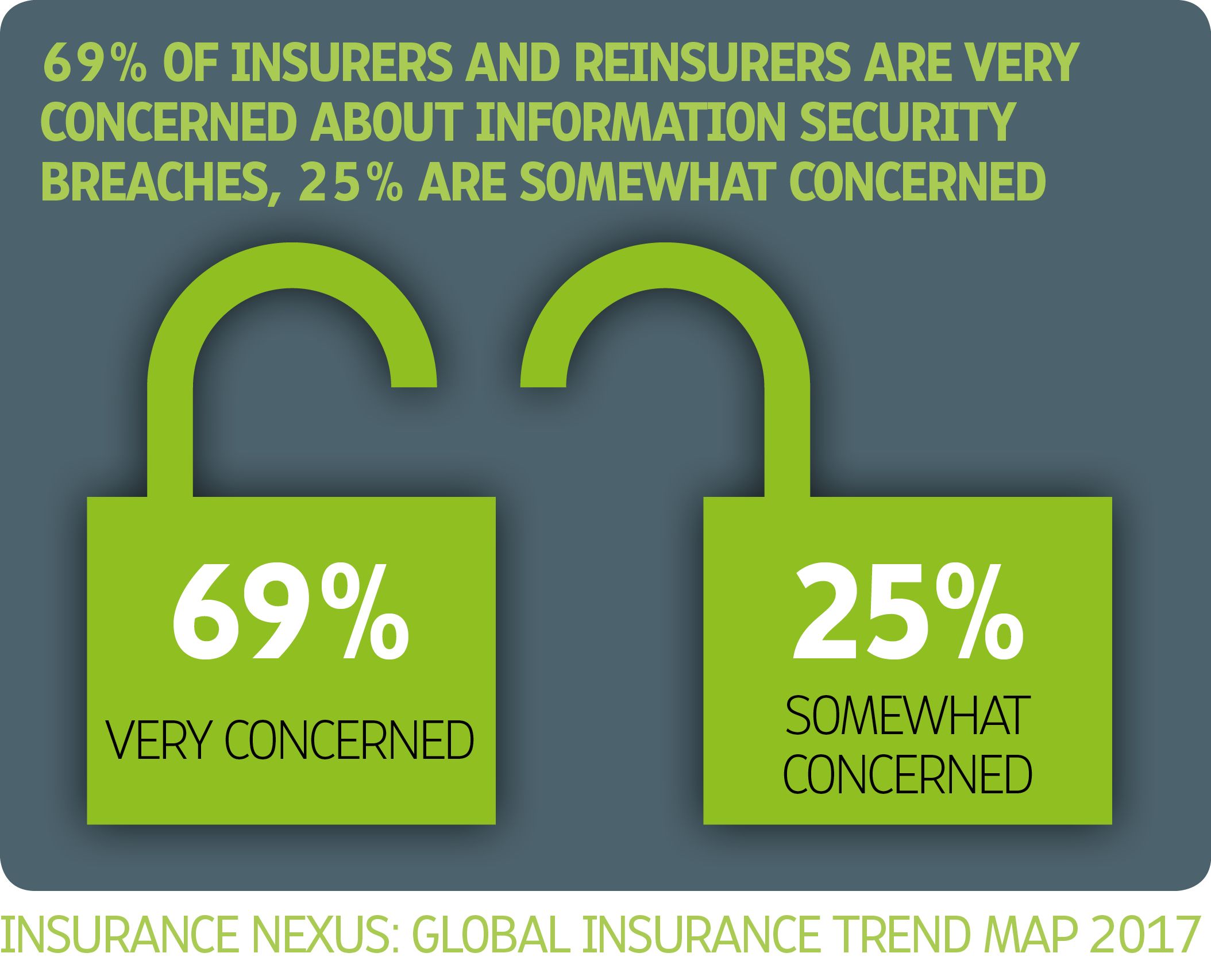

This year's Global Trend Map did not contain a dedicated section on Blockchain, but we look forward to including one in our 2018 edition, so stay tuned! In our next installment we move on to the germane topic of Cybersecurity: considering what insurers can do to keep their vast troves of customer data safe from attack. Or, if you'd like to read ahead straight away, then simply download the full Trend Map whenever you like.

For any inquiries relating to the Insurance Nexus Global Trend Map, this on-going content series or next year's edition, please contact:

Alexander Cherry, Head of Research & Content at Insurance Nexus (alexander.cherry@insurancenexus.com)