Insurtech has come to age, a bunch of the oldest insurtech players has been acquired or listed.

Over the last 24 hours, we have seen:

- Travelers acquiring Trov: https://www.insurancejournal.com/news/national/2022/02/23/655414.htm

- Lemonade and Root publishing their financial numbers

I love numbers, and I've crunched insurtech financial numbers for the past few years.

Lemonade has written almost $370M premiums (showing a 42% growth from 2020) and Root has written more than $740M premiums (showing a 20% growth from 2020)

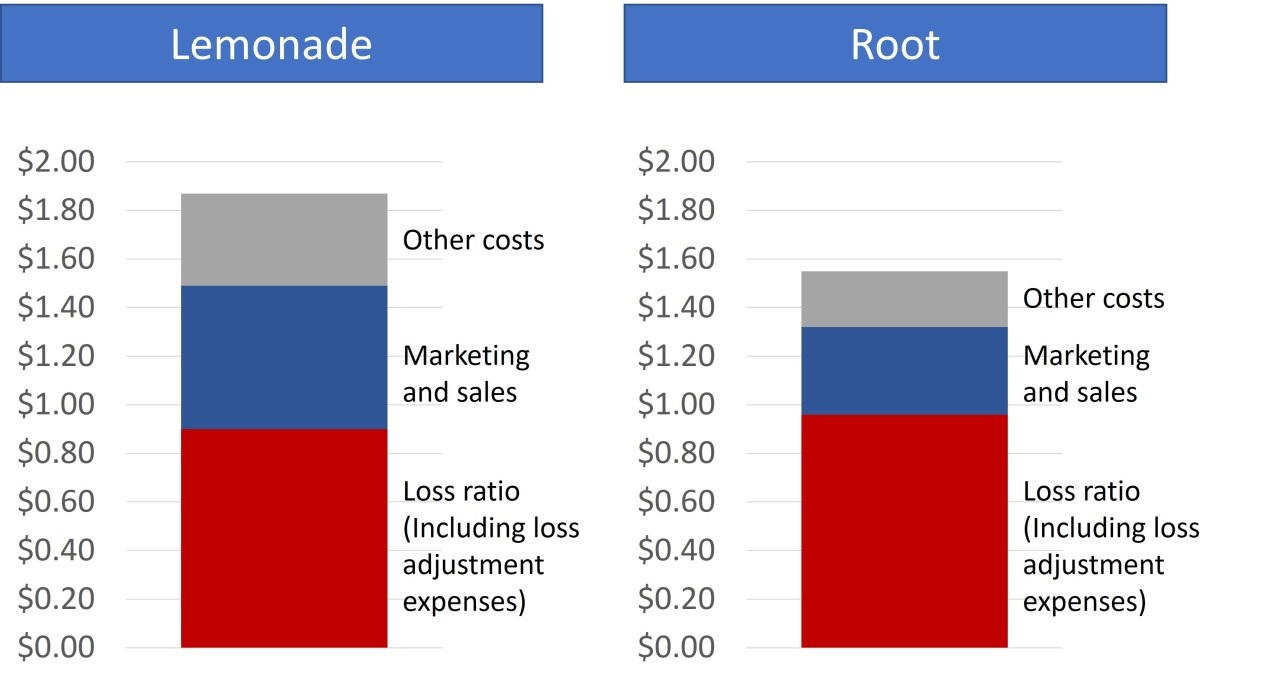

However, both these two full stack insurtech players have run an insurance business with a combined ratio (gross of reinsurance) above 150% combined ratio in 2021. This means that for each dollar of premium paid by the client their risk transfer approaches a cost of more than 1.5$.

Almost the same has happened over the past three years.

How it started

We all remember how Lemonade has fascinated the healed and conquered the soul of insurance professionals:

Lemonade CEO interview in 2017:

“Many industry-insiders think so, too: ‘At least 40% of what insurance carriers receive in premiums Insurance carriers is paid out in claims. So if Lemonade is 80% cheaper it must lose money on every policy.’ That is not true. Renters insurance covers personal property, not real estate. The expected loss is therefore significantly lower and so should the corresponding premium be. Unfortunately, the enormous overheads incumbents have, make low premium products impossible. Their minimum premium reflects their high costs rather than your low claims.”

"We apply behavioural economics to neutralise the adversarial relationship, the conflict of interest, between customers and their insurance provider. We take 20% and the rest (80%) goes to paying claims, and this includes our reinsurance. If less than the 80% is used to pay out claims, for instance 75%, the 5% unclaimed money is donated to charities chosen by customers. The maximum amount that can be given back is 40%. Lemonade gains nothing by refusing a claim. This way we are reinventing insurance from a necessary evil to a social good."

Moreover, on their blog:

"That changes everything. Insurers typically make money by investing premiums (“float”) or by paying out less in claims and expenses than they took in premiums (“underwriting profit”). Lemonade relies on neither. We collect premiums monthly, so the money earns interest in your bank account, not ours, and we return unclaimed money at year’s end in Lemonade’s Giveback.

Knowing you’re not in conflict with your insurer, and that you embellish claims at the expense of a cause you believe in, may change your behavior too, setting off a virtuous cycle. Ultimately we’re after a new Nash equilibrium, one where aligned interests breed trust, resulting in a product that is inexpensive, hassle-free and lovable."

Over these years, I've been pretty skeptical about this storytelling:

...and I have challenged a few times the sustainability of their financials.

They didn't like it so much.

How it's going

Let's start with the giveback (the data about the 2021 business have not yet been disclosed):

$2.3M give back accounts for 1 cent on each dollar of written premium. Pretty different from the expectation given by the iconic pizza slice that characterized their storytelling back in the days.

Let's look at the financials. For each dollar of premium, claims cost 90 cents including the loss adjustment expenses (it seems that old claims have been underserved, well we could discover in 12 months that even the current year reserves are not adequate). To acquire this (underpriced?) business they invested almost 60 cents in marketing for each dollar of premium. Last but not least, all the other costs amount to almost 40 cents.

It doesn't seem that behavioral economics, charity..and storytelling have made any dent in the insured risks.

So, all the insurance professionals - who fell in love with their disruptive storytelling over the past 6 years - should feel a little betrayed ...here, I see no more that a fantastic team, driving a superb marketing machine, with a cool front-end ... selling online (but even on this distribution approach, some signs of change -> at page 6 they share the usage of independent agents).

No sign of disruption, or at least not yet.

Want more numbers?

Join the 15.000 insurance executives who have already subscribed to the

Insurtech Facts & Figures newsletter

-------------------

Article originally published on Linkedin:

https://www.linkedin.com/pulse/do-you-feel-betrayed-matteo-carbone/