The ability to accurately discern the past and predict the future based on nothing but data points and the experience of actuaries and adjusters has served the industry well up to now. Insurance is, after all, a multi-billion-dollar, truly global industry. While this remains the case, the landscape is now radically different to the past, thanks in part to the advent of the Internet of Things (IoT). The use of these technologies that collect, record and transmit live data has proliferated exponentially over the past decade, and for a data-reliant industry like insurance, the impact has already been profound.

They may already seem ubiquitous but estimates of how many IoT devices will connect our cars, homes, communities, medical services and work lives by the year 2020 range from 30 billion[i] to 50 billion[ii]. Whatever the precise number, this will generate (and already is) a huge amount of data to be analyzed and monetized.

This increase in the quality and quantity of available data is already producing some significant outcomes; the process of writing policies can now be far better informed by what is known about the risk level of an individual or entity, as opposed to simply what is known about the claims generated by an entire class of risk. Some carriers have already begun this transition; John Hancock, for example, announced in 2018 that all new life insurance policies must henceforth use digital fitness trackers to monitor policyholders[iii]. Using the high-quality, objective data derived from IoT, it is now possible to assess claims more accurately and efficiently, and in some cases, even prevent them from arising entirely.

“IoT is already enabling customers to avoid bad things happening to them. Some people call it prevention. I see it as empowerment of customers.” – Nick Ayrdon, Head of Strategy & Development at Aviva

In turn, this is changing how insurers interact with customers, both before and after a claim, with one executive predicting that that we are in fact “shifting from a claims-handling business to a claims prevention one”. As the value proposition of exchanging data for value becomes more concrete, it could become a strong pull-factor driving uptake of connected insurance products. And yet, already operating in an environment of squeezed profits, high regulation and low consumer trust, the industry is witnessing something of a perfect storm at present.

There is no question as to whether the global insurance industry is going to go digital, and most of the industry understands why it will. The real problem for most is how it should happen and creating an environment in which they can maximize the value of insurance technology. As Michael Lebor states, this is not simply a case of reorganizing a particular department or function: “In my opinion, IoT is not a product, it’s a paradigm shift, a completely different way for technologies to interact with each other. Devices are going to be talking to each other, there are going to be hubs, and we must leverage that throughout the entire lifecycle of our product, whether for distribution, or on-boarding customers, or using it for claims and first notice of claims. It’s not one product, it’s a holistic way of thinking.”

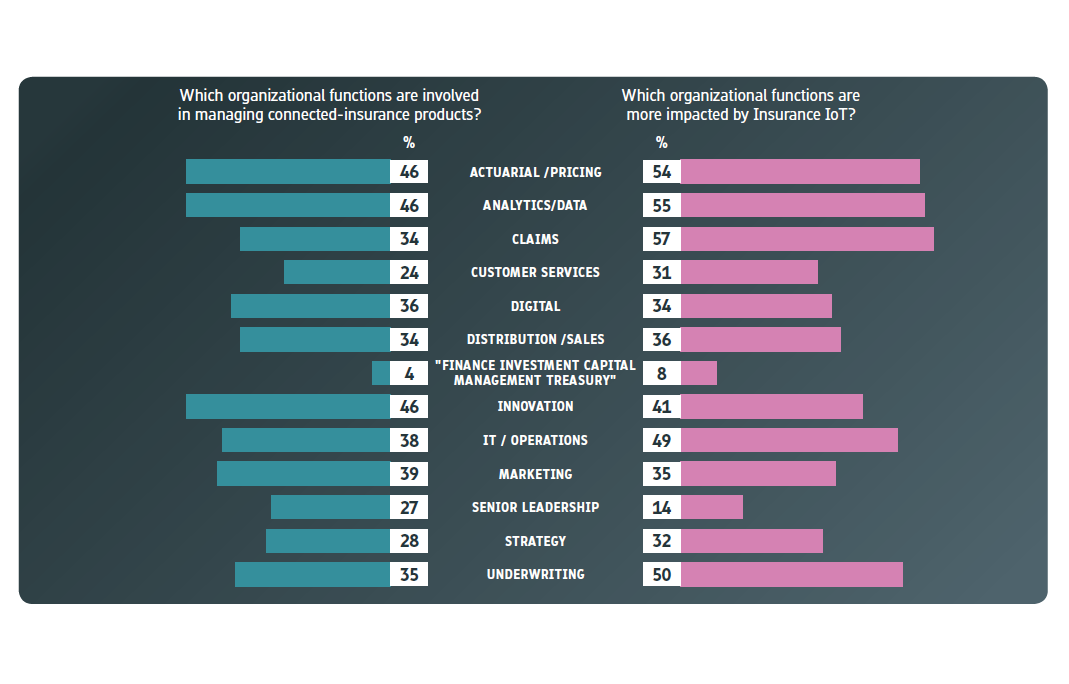

Any transformation of this nature will invariably lead to substantive changes in how insurance carriers operate internally and whereas digital insurance projects were generally siloed to innovation departments in the past, executives agree that is starting to change. While the survey found that only 14% of senior management teams were currently affected by the introduction of insurance technology, the most commonly cited reason was that initiatives had not yet reached the point where it had become necessary (the implication being that management will take a more active stance when projects have scaled sufficiently).

Similarly, American Family Business Development Manager, Shaun Wilson, suggests “until there are a lot of devices providing a lot of data about specific risks, the carrier is not going to have the insights about whether or not these devices mitigate risks to any level of significance. That’s the promise of this approach, but nobody has enough data yet to validate the hypothesis.” As carriers leverage connected technology more and the impact on the business deepens, however, we can expect to see greater top-down management and involvement from board level stakeholders[iv].

To provide a comprehensive overview of the progress and prospects of Connected Insurance, Insurance Nexus have produced the Connected Insurance Report, an in-depth study of the progress of insurance technology globally, today, and in the future.

As the industry begins to understand how it can exploit the possibilities of connected and insurance technology, the Connected Insurance Report has crystalized the concerns of those tasked with turning an unprecedented technological revolution into market-ready products. At first glance, one might assume that the ability to learn more about the risks they are insuring should allow both for policies to closely follow the risk over time, and secondly that the ability to gather more information about a claim will discourage fraud. The net result should therefore be greater profit for companies, and lower premiums for their customers.

At second glance, it is just as clear that the picture is much more complicated than that. As we talked to more and more executives, it became apparent that the industry is only just beginning to work through the practical problems it faces. Indeed, questions as basic as the best way to install a sensor in a building are still the subject of lively debate. Ultimately, the world of insurance may be next in line for the kind of creative destruction that the tsunami of digitisation had brought to IT, telecoms, media, retail, hospitality, manufacturing, financial and business services.

The Connected Insurance Report was researched and produced by Insurance Nexus in collaboration with the IoT Insurance Observatory. It is the first of its kind to conceive of insurance IoT holistically, as a paradigm shift necessitating changes in insurer business models, organisational structures and technology stacks. Insurance Nexus surveyed the experiences of more than 500 insurers and reinsurers to assess where they sit in the connected insurance market and to extract the challenges they face and their stories of success.

Along with a panel of 20 industry leaders who have been operating at the sharp end of the IoT revolution, Insurance Nexus looked at these hurdles and opportunities and pulled them apart to provide readers with the case studies with actionable insights to help guide decision-making as the industry tackles its own strategic milestones.

--

[i] https://spectrum.ieee.org/tech-talk/telecom/internet/popular-internet-of-things-forecast-of-50-billion-devices-by-2020-is-outdated

[ii] https://www.accenture.com/gb-en/insight-insurance-internet-things

[iii] https://www.bbc.co.uk/news/technology-45590293

[iv] https://assets.kpmg/content/dam/kpmg/xx/pdf/2019/03/insurtech-trends-2019.pdf