Is telematics changing the motor insurance market by disrupting the traditional car insurance business model ?

The paper published by Swiss Re tries to answer this question by looking at the Italian market which is known for having the highest coverage of telematics-based motor policies worldwide and which can serve as a benchmark for replication in other markets. The aim of the paper is to show how insurers and consumers can profit from the value proposition of telematics, how telematics is changing the motor insurance landscape with a deep dive into latest technical data.

Digitalization together with innovative technology have triggered a shift in the automotive industry in the last 10 years, with traditional cars already having semi-autonomous features and a tendency of moving towards fully autonomous vehicles in the future. The spread of telematics is the main underlying driver for innovation in the automotive industry. The paper defines telematics as “a combination of computers and wireless telecommunication technologies to facilitate an efficient transfer of information over vast networks”. The actual starting point was in 1988, when the European Economic Community launched programmes that were experimenting with motor telematics, and ten years later you could see “progressive Insurance” in the US and the first issued telematics policies. Even so, telematics only recently started to have an important market penetration which in Italy’s case has reached 15–16% of all motor insurance policies at the end of 2016. This is the equivalent of 6.3 million policies which confronted with the 4,8 million active telematics policies at the end of 2015 is a clear sign that the market is preparing itself for the adoption of such solutions on a larger scale.

Source: Matteo Carbone, 2015

As illustrated in the above image, Italy is ahead of the US (3.3 million) and the UK (0.6 million). Compared to the US, where dongles were the main data source at the end of 2015, the black box was the main device used for collecting data in combination with telematics-based motor policies in Italy and the UK.

A major implication of telematics is that it allows cars to communicate with each other and with the overall infrastructure. So it could just be that in the future two vehicles will be capable of warning each other of obstacles or hazards on the road and cars can be re-routed by intelligent traffic signs. Complementary to telematics technology, there are advanced driver assistance systems (or ADAS), a major step in the race towards completely autonomous vehicle with Volvo, Daimler and Tesla leading the way. ADAS typically includes safety enhancing features, such as emergency brake assist (EBA), side-view (blind spot) assistance, forward collision and lane departure warning systems. The Mercedes Model S is fitted with several sensors that read the road ahead to adjust steering, speed and brakes. Meanwhile, the software installed in Tesla’s Model S enables driving with an autopilot on US highways. Various other car manufacturers have built emergency auto-brake functionality into their cars.

The opportunities for the insurance sector brought by ADAS and telematics technologies are several, all related to road safety. Data shows how technology assisted and autonomous driving will cut the frequency and costs of road accidents, which are mostly caused by human error (>90%).

The true value of telematics is in the data, which are transformed into actionable knowledge affecting all components of the insurance value chain. This has brought unprecedented levels of innovation to motor insurance, a part of the insurance industry which is traditionally adverse to change.

Debate on the connected #insurance paradigm for a connected generation with @MCins_ @pisarzp @halesinspain @SwissRe #FTSMI17 #insurtech pic.twitter.com/7VE9gPayAC

— Insurtechnews (@insurtechnews) May 5, 2017

According to the paper, the impact of telematics on motor insurance is reflected in several areas such as risk selection (which can enable insurers to select and price risks more accurately), more efficient claims handling processes and reducing loss frequency (reduction in expected losses for insurers and overall decrease of insurance premiums for drivers). Although there is not yet any strong statistical evidence about changed or improved driving behavior for customers with telematics-based insurance policies, the analyzed data indicates a positive trend that this will be the case in the near future. However, the report links this to the need for advanced premium schemes, such as Pay-how-you-drive.

The paper identifies three key points of the value proposition for insurers, resulting from ‘connected insurance’:

- Frequency of interaction, which enhances proximity with the customer and is aimed at offering;

- Benefits to the insurance bottom line, resulting in increased profitability through specialization (includes the ability of a telematics-based offering to auto-select risks, influence driving behavior and use collected data efficiently during the claims handlings process)

- Knowledge creation on risks and customers, based on a combination of car data and contextual data, which will allow the development of new risk models and the identification of cross-selling opportunities.

These benefits are prompting insurance companies to innovate their traditional approach and to come up with their own telematics strategies, from customer acquisition to customer retention and cross-selling, to improve the portfolio’s profitability. Going a step further, telematics applied, for example, to car sharing can also positively affect traffic conditions and air quality, by making more efficient use of resources.

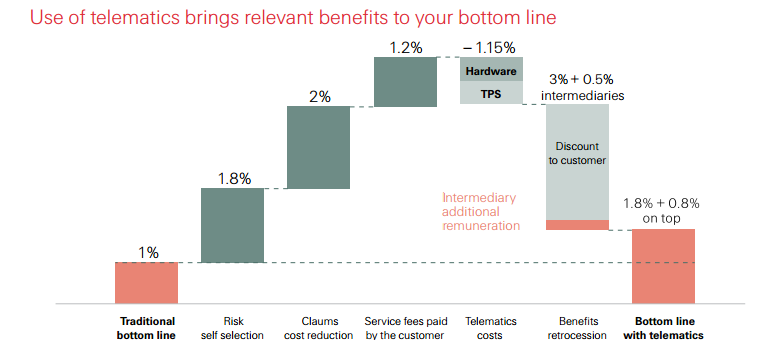

Telematics potentially provides the mechanism required to prevent that a decrease in premium automatically translates into lower profitability. According to the paper’s authors the above-mentioned success factors, if activated correctly, will bring net value generation, allowing lower premiums to co-exist with profitability. “The key element of this approach – highlights Matteo Carbone, contributor to the paper - is the value generated by leveraging telematics data and sharing this value with the customer”. The comparison between the traditional insurance bottom line and the telematics-based insurance bottom line shows that risk self-selection, claims cost reduction and service fees paid by the customer generate more benefit than the loss resulting from discounts, premiums and costs for third-party suppliers (see below graph). However, insurance companies have to develop business cases which achieve this profitable telematics-based bottom line.

Source: Matteo Carbone, 2016

The paper identifies five value creation levers for insurers:

a) Risk selection - low risky customers acquisition and connected reduction in fraudulent intents Underwriting process quality improvement

b) Risk-based pricing - usage Based Insurance: pricing definition process based on “quantity” and “level” of risk exposure

- concerning policy information

- having high value added for drivers

- related to insurance cross-selling and products connected to the insurance contract

d) Loss Control

- proactive intervention for claims management

- objective information about incidents

- use of value-added services in order to mitigate the risk/ prevent the loss

e) Loyalty and “behavior steering”- loyalty systems based on detected customer driving behavior

- positive behavior reinforcement

- gamification

For a detailed explanation of the above-mentioned concepts, you can refer to pages 20 and 21 of the original paper available here.

The insurer can benefit from a series of positively impacting results related to the use of telematics and connected insurance, but what about the customer? What is the insured’s point of view?

ANIA conducted a research together with companies from the Italian market and discovered that discounts offered with installed telematics attract customers of all ages. Although young drivers aged between 18 and 23 have the highest interest in telematics-based insurance policies combined with a black box, further results show that all customer segments reached a material penetration and are increasingly opting for those policies.

In 2015, 5% of all motor insurance customers decided to move from a traditional motor insurance to a black box-based insurance policy, while overall retention of such customers seems to be increasing over time. Customers perceive that telematics has advantages as they identify lower premiums, enhanced safety and improved claims experience, as top incentives in choosing a telematics-based UBI.

A recent survey conducted by Survey Sampling International (SSI) for the Connected Insurance Observatory in 2016, surveyed 3525 customers in seven countries (Austria, France, Germany, Italy, Spain, UK, US). Their findings confirm that price is the most important factor for customers choosing a motor insurance product, while the second is the array of services offered by the insurance company.

Apart from the possibility of reducing premiums and making claims handling processes easier, customers with a device or smartphone app installed are able to benefit from a variety of value-added services, such as roadside assistance, help in case of an emergency and recovery of stolen vehicles. The surveyed participants ranked several value-added services based on their perceived attractiveness. Even though country-specific preferences differ, anti-theft services, easier claims handling and a car locator feature are highly appreciated across all surveyed countries. Parental control and personalized non-insurance offers are of the least interest among participants.

"The Italian market has developed the furthest in terms of telematics penetration, and the evidence and experiences collected should be seen by all as bearing significant relevance. Best practices are and will be collected in early adopter markets, like Italy, to be tested and (partly) replicated elsewhere", said Daniele Del Bo, Growth Project Manager and Vice President Europe, Middle East & Africa at Swiss Re.

To conclude, the popularity of telematics has increased rapidly in Europe, driven mainly by Italy, and UBI subscriptions are expected to take off in the UK, Germany and France within the next five years. Other areas, such as property, life and health are showing signs of change, as connected cars, connected homes and connected lives could merge into a connected ecosystem protected by connected insurance. Even if cyber risk is also part of this “connected world” the interest for this type of technologies is ever increasing while investments keep pouring in.

"The full paper 'Unveiling the full potential of telematics' is the result of ajoint collaboration between Swiss Re, Matteo Carbone, Sergio Desantis and Gianni Giuli. The discussions triggered by this work were instrumental in improving the understanding of the topic.", added Del Bo.

The paper can be downloaded at this link: http://www.swissre.com/library/archive/unveiling_the_full_potential_of_telematics_how_connected_insurance_brings_value_to_insurers_and_consumers.html#inline