The insurance sector is undergoing a profound change. Digital transformation has become a major challenge for insurance companies all over the world.

In Italy, this transformation is exemplified by the adoption of vehicle telematics. According to the latest IVASS data, black box became an integral part of 15.5% of new policies and renewals during the third quarter of 2015.

Auto #insurance #telematics mainstream in Italy: penetration >15% [Click to Tweet]

The insurance sector is now seeing the same dynamics already experienced inmany other sectors, including financial services: with startups and other tech firms innovating one or more steps of the value chain traditionally belonging to financial institutions. InsurTech has seen investments of almost $2.65 billion coming in during 2015 compared with $0.74 billion in 2014. Similar to FinTech in 2015, it’s now InsurTech’s turn to define the elements to be included in the observance perimeter, this being a main point of debate among analysts.

In my opinion, all players within the insurance sector will have to become InsurTech-centered in the coming years. It’s unthinkable for an insurance company not to pose the question of how to evolve its own model by thinking which modules within their value chain should be transformed or reinvented via technology and data usage. Realizing this digital transformation can be achieved by building the solutions in-house, by creating partnerships with other players—both start-ups and incumbents—or through acquisitions.

All the players in the insurance arena will be InsurTech. [Click to Tweet]

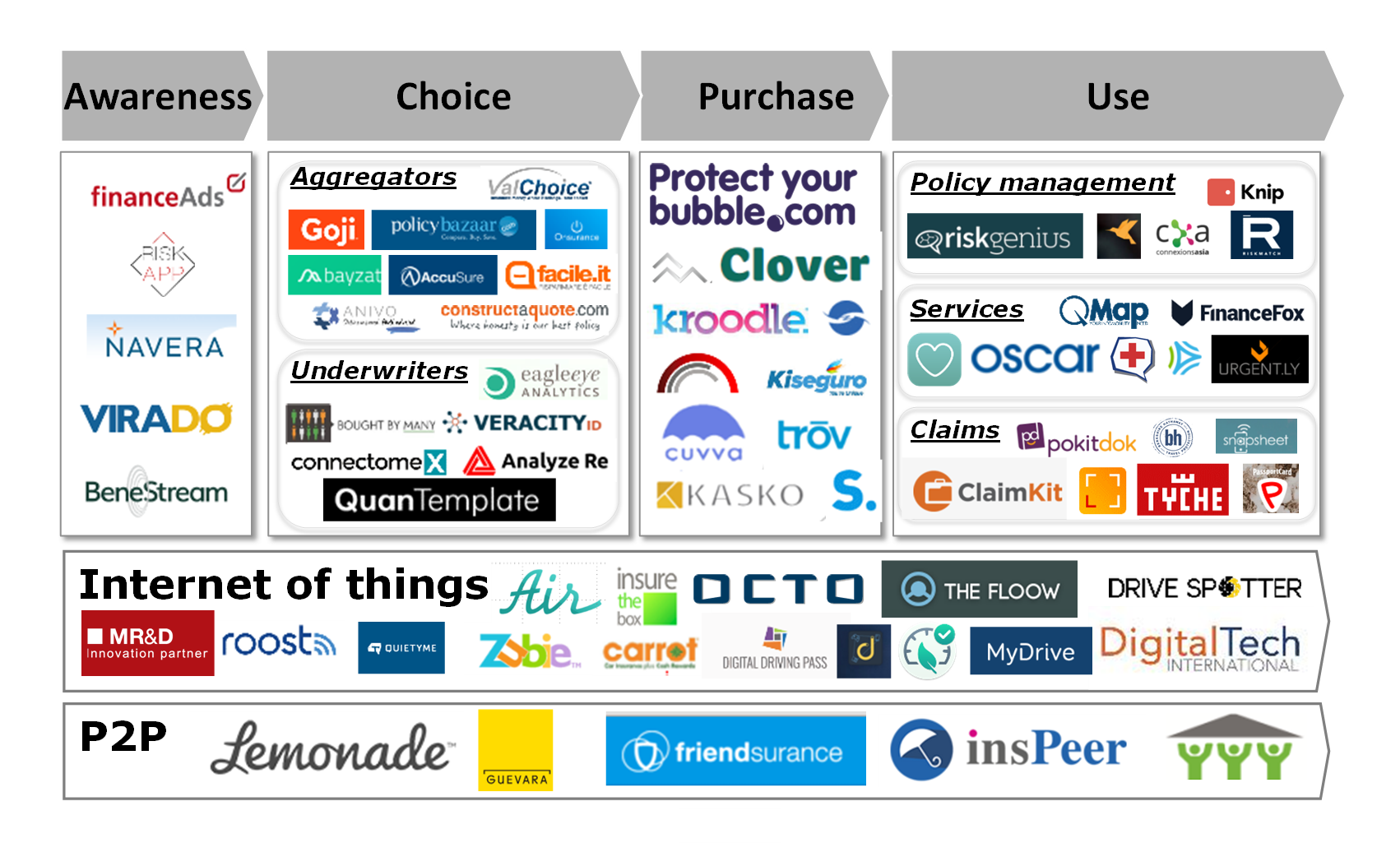

Based on this view that all the players in the insurance arena will be InsurTech—meaning organizations where technology will prevail as the key enabler for the achievement of strategic goals—the way to analyze this phenomenon is via a cross-section view of the customer journey and the insurance value chain. This mental framework, which I regularly use to classify every InsurTech initiative—whether it’s a start-up, a solution provided by established providers or a direct initiative by an insurance company—is based on the following macro-activities:

- Awareness: Activities that generate awareness in the client—whether person or firm---regarding the need to be insured and other marketing aspects of the specific brand/offer;

- Choice: about an insurance value proposition, which, in turn, are divided into two main groups:

- Aggregators, who are characterized by the comparison of a large number of different solutions;

- Underwriters, who are innovating the way to construct the offer for the specific client, irrespective of the act to compare different offers.

- Purchase: Focuses on innovative ways in which the act of selling can be improved, including collection of premiums;

- Use of the insurance product: clarifies three very distinct steps of the insurance value chain: policy handling, service delivery—which is acquiring an ever-growing significance within the insurance value proposition—and claims management;

- Recommendation: Part of the customer journey which is becoming a key element in the customer’s experience with a product in many sectors;

- The Internet of Things (IoT), we can include in this category of activities—transversal to the activities described above—all the hardware and software solutions representing the enablers of the connected insurance (the motor insurance telematics is the most consolidated use case):

- Peer-to-peer (P2P): Initiatives that, in the last few years, have started to bring peer to peer logic to the insurance environment, in a manner similar to the old mutual insurance.

- on the one hand, there is a tendency towards ecosystems in which each value proposition becomes the integration of multiple modules belonging to different players;

- on the other hand, the lines between the classical roles of distributor, supplier (coming even from other sectors), insurer and reinsurer are getting blurred.

In a scenario like this, the balance of power (and consequently the profit pool) among various actors is bound to be challenged and each one of them may well choose to collaborate or compete depending on context and timing.

My friends of InsurTech News represented - based on my framework described above - a map of the InsurTech newcomers and will continue to map the most interesting initiatives. Please feel free to comment adding more InsurTech newcomers you know.