The use of the blackbox for insurance risk selection was one of the first drivers that help spread the motor insurance telematics solutions, but this approach is now taking new and innovative forms

The fusion between car insurance policies and telematics solutions and the possibility for innovation in this respect is right now one of the main focus points for all big international level Insurance Groups . Years of experimenting have shown how the installation of a box on an automobile can be harnessed to bringconcrete benefits in the insurance value chain.

The evolution of this technology, along with the exponential growth of data management and analysis capacity, opens up a whole new range of opportunities to innovate the traditional insurance approach: this calls for a serious and strategic reflection on behalf of all insurance companies on how to come up with their own telematics approach.

Based on that, one can state that motor insurance telematics is still at an incipient stage—even in Italy where market penetration is above 8%—and in order to see it grow on a larger scale, the implementation of approaches that manage to exploit its full potential, is required.

Looking at the big picture of the more international innovative approaches it becomes clear how every Insurer has the concrete opportunity to finalize this innovation effort in that which regards its own business priorities starting from customer acquisition and leading to retention, or from improving the portfolio’s profitability to cross-selling.

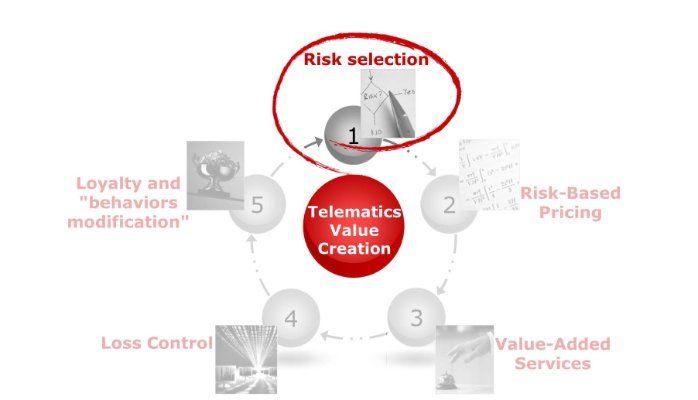

As follows, a scheme I usually use when offering support to insurance companies by providing strategic insight into the telematics sector and which articulates the approach towards innovation in 5 distinct areas:

- Risk selection

- Usage-based insurance (UBI)

- Added value services

- Loss control

- Loyalty and behavior steering

These five areas represent the levers which one might activate in order to harness the full potential of this technology and to maximize the ROI of telematicsinitiatives.

Risk selection

This category is comprised of all those approaches that allow a risk selection in the new client acquisition phase or when renewing a policy: on the one hand, they are solutions meant to take advantage of the autoselective and dissuasion of risky behavior capacity, which typically characterize a product based on the installation of a box that is meant to monitor behaviors and to reconstruct the dynamics of the claims; on the other hand they are meant to integrate the static variables, which are traditionally used, with a set of “telematics data” collected for a limited period of time, with the sole purpose of supporting the underwriting phase.

In Italy, the first types of car insurance policies to be introduced were the ones working in conjunction with the black-box but without having a pricing based on telematics variables—still today they represent little less than half of the 34 telematics solutions present on the Italian market. This type of solution, in most of the cases, is commercially presented as an optional feature which can be activated on a traditional car insurance policy for which there is a corresponding flat discount for the motor guarantees.

At an International level the most consolidated and best know approach when it come to risk selection is Snapshot by Progressive —one of the main USA insurance companies—which has been used over the years in approximately 14% of the overall auto portfolio of the Company. By using a telematics box for a period of 75 days, the client gets a price adjustment based on his or her own style of driving: for many years this was just a simple discount—which is an improvement to the traditional tariff—whereas in recent months there has been an additional price increase for drivers that display risky behavior. Progressive thus uses a temporary behavior tracking approach, using the rollover technique which is based upon the concept of lending the box (a self installing OBD dongle ) to the client per 75 days in which the telematics data are collected and subsequently intercepted by the Company.

An interesting example of innovation in the use of telematics for risk selection purposes is given by Safeco Rewind of the American group Liberty Mutual. In this case the box-related approach had been used to deal with the problem of after-claim client retention, which typically find themselves with a rise in the premium. The company offers to all clients that have had a crash, the possibility to install a temporary self-installing device which detects the style of driving: when the client renews the policy and gives back the box, if the registered behavior is proved to have been a cautious one, then the increase in the premium/rate is limited or in some cases is completely absent in spite of the claim.

This article originally appeared in the Insurance Daily n. 719 edition.